Getting My Mortgage Investment Corporation To Work

Getting My Mortgage Investment Corporation To Work

Blog Article

The Main Principles Of Mortgage Investment Corporation

Table of ContentsThe Definitive Guide to Mortgage Investment CorporationSee This Report on Mortgage Investment CorporationExcitement About Mortgage Investment CorporationMortgage Investment Corporation Can Be Fun For AnyoneMortgage Investment Corporation Can Be Fun For Everyone

Does the MICs credit rating committee evaluation each home mortgage? In most situations, home mortgage brokers take care of MICs. The broker needs to not work as a participant of the credit scores committee, as this puts him/her in a straight dispute of interest considered that brokers normally make a commission for putting the home mortgages. 3. Do the supervisors, participants of credit history committee and fund manager have their very own funds invested? A yes to this inquiry does not supply a risk-free financial investment, it should supply some boosted safety if assessed in combination with various other prudent financing policies.Is the MIC levered? The monetary establishment will approve particular home mortgages had by the MIC as safety for a line of credit scores.

This should offer for additional examination of each mortgage. 5. Can I have copies of audited monetary declarations? It is essential that an accountant conversant with MICs prepare these statements. Audit procedures must make sure rigorous adherence to the plans mentioned in the details package. Thanks Mr. Shewan & Mr.

The Best Guide To Mortgage Investment Corporation

Last upgraded: Nov. 14, 2018 Few investments are as advantageous as a Mortgage Financial Investment Company (MIC), when it concerns returns and tax benefits. As a result of their company structure, MICs do not pay earnings tax and are legally mandated to disperse all of their revenues to financiers. In addition to that, MIC dividend payouts are treated as interest earnings for tax functions.

This does not mean there are not threats, however, generally speaking, no issue what the wider stock market is doing, the Canadian property market, especially major cosmopolitan areas like Toronto, Vancouver, and Montreal carries out well. A MIC is a firm created under the rules set out in the Earnings Tax Obligation Act, Section 130.1.

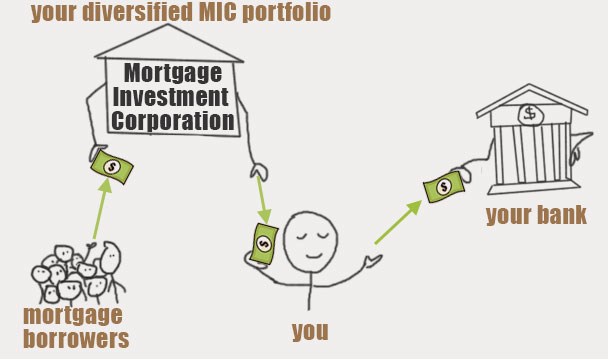

The MIC makes revenue from those mortgages on passion fees and basic fees. The genuine allure of a Home mortgage Financial Investment Corporation is the yield it supplies capitalists compared to other fixed revenue investments. You will have no problem locating a GIC that pays 2% for a 1 year term, as federal government bonds are similarly as reduced.

The Buzz on Mortgage Investment Corporation

A MIC must be a Canadian corporation and it must invest its funds in mortgages. That said, there are times when the MIC ends up possessing the mortgaged building due to repossession, sale arrangement, etc.

A MIC will certainly make rate of interest earnings from mortgages and any type of money the MIC has in the financial institution. As long as 100% of the profits/dividends are offered to shareholders, the MIC does not pay any kind of earnings tax. Rather of the MIC paying tax obligation on the interest it gains, shareholders are accountable for any type of tax.

Not known Incorrect Statements About Mortgage Investment Corporation

And Deferred Strategies do not pay any tax obligation on the rate of interest they are internet estimated to get - Mortgage Investment Corporation. That stated, those who hold TFSAs and annuitants of RRSPs or RRIFs might be hit with specific penalty taxes if the investment in the MIC is taken into consideration to be a "restricted financial investment" according to Canada's tax code

They will certainly ensure you have actually found a Home loan Financial investment Corporation with "certified investment" condition. If the MIC certifies, maybe extremely advantageous come tax obligation time given that the MIC does not pay tax on the rate of interest income and neither does the Deferred Strategy. A lot more extensively, if the MIC falls short to meet the demands established out by the Income Tax Act, the MICs revenue will be strained prior to it gets distributed to investors, lowering returns dramatically.

It shows up both the realty and securities market in Canada go to all time highs On the other hand yields on bonds and GICs are still near record lows. Also money is losing its charm because power and food prices have pressed the inflation price to a multi-year high. Which asks the concern: Where can we still locate value? Well I assume I have the answer! In May I blogged regarding checking out home loan financial investment corporations.

Indicators on Mortgage Investment Corporation You Should Know

Many hard functioning Canadians that desire to purchase a home can not get home loans from conventional banks since maybe they're self utilized, or don't have an established credit report background. Or perhaps they want a short term loan to develop a big building or make some renovations. Financial institutions often tend to overlook these prospective customers because self used Canadians do not have stable revenues.

Report this page